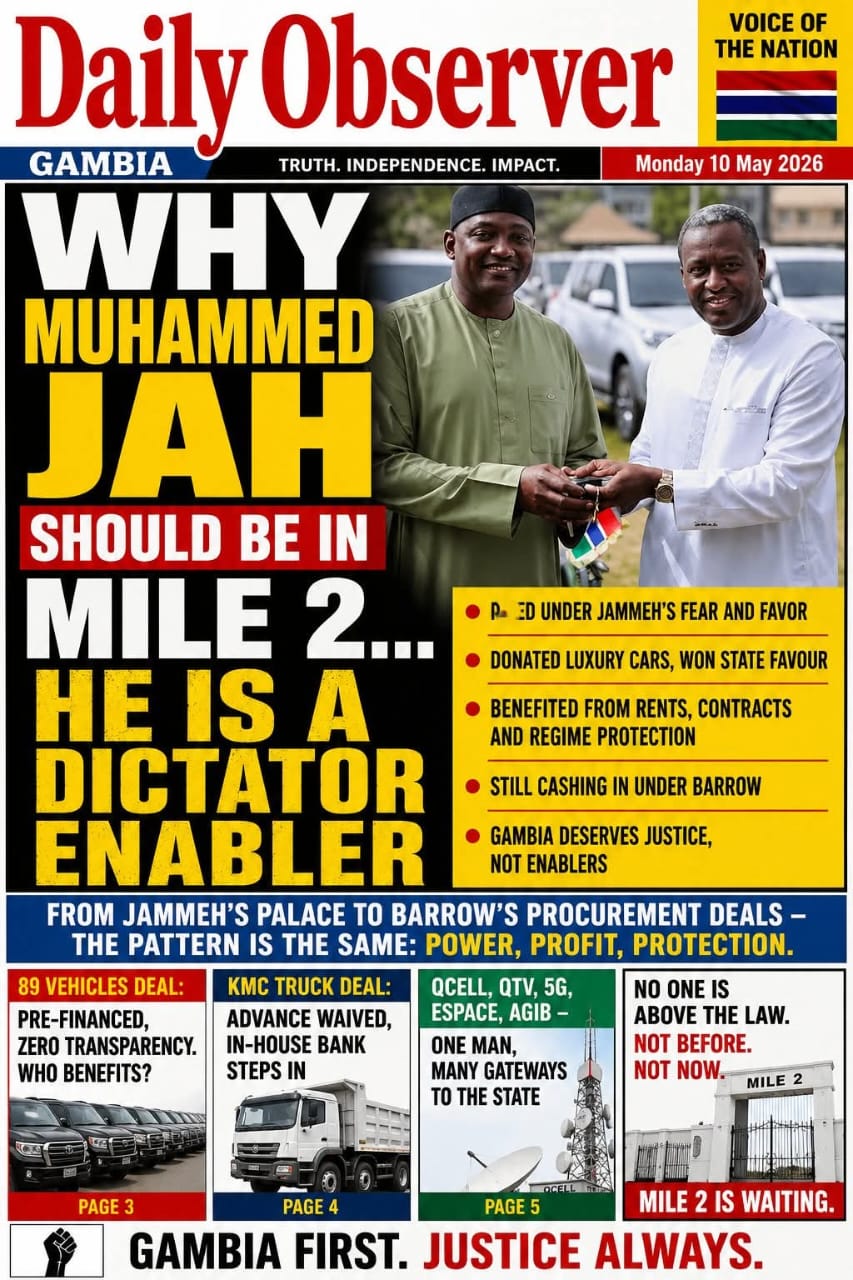

MUHAMMED JAH: THE ECONOMIC VAMPIRE WHOSE EXPANDING EMPIRE IS CRIPPLING AND DEVOURING GAMBIAN BUSINESSES

There is an old saying in political economy that in weak states, markets rarely reward the most innovative entrepreneur. Instead, they reward the man who stands closest to power. In modern Gambian capitalism, few figures embody this uncomfortable reality more visibly than Muhammed Jah, the dictator enabler.

Jah’s commercial ascent from the obscure world of dial-up internet provision to the commanding heights of telecommunications, broadcasting, procurement and banking demonstrates this with almost mathematical precision. Jah’s transformation from the proprietor of QuantumNet, one of The Gambia’s earliest private internet providers, to the owner of QCell, QTV, Espace Motors, and a broader commercial network is therefore more than a corporate success story. It is an illustration of how weak institutions, discretionary regulation and political intimacy can accelerate the concentration of private capital in small African states.

To his admirers, Jah is a patriotic entrepreneur who rose from humble beginnings to become one of the country’s most recognizable investors. To his critics, however, he represents something far more troubling: the emergence of a politically connected oligarchic class that prospers not merely through innovation but through strategic proximity to successive governments.

The issue is therefore not whether Muhammad Jah is intelligent, hardworking, or commercially ambitious. He clearly is. The issue is whether the Gambian economic system has become structured in such a way that one businessman repeatedly enjoys regulatory flexibility, procurement access, symbolic presidential endorsement, and financial accommodation unavailable to ordinary investors.

Since the early 2000s, several once-prominent Gambian business houses either declined, stagnated or lost strategic relevance. Jimpex Trading, associated with Hatib Janneh once occupied a major commercial position within the country’s trading economy. Gacem, linked to Amadou Samba, similarly carried substantial economic weight. Unique Solutions associated with Papa Yusupha Njie also emerged as a recognizable force within Gambian commercial life.

Yet while many of these firms gradually contracted, stagnated or disappeared from prominence, the Jah business orbit continued expanding aggressively across sector after sector. In mature economies, such patterns would trigger anti-trust scrutiny, parliamentary hearings and aggressive media investigation. In weaker economies, however, the market often behaves less like a competitive exchange floor and more like a closed political trading ring where insiders accumulate privileged leverage while outsiders remain trapped outside the corridors of influence.

Regime Proximity from Jammeh to Barrow

The criticism that Jah “sides with every government” should be stated more carefully but not diluted. The public record shows opportunistic regime adaptation. Under Jammeh, Jah was not a silent operator. A 2013 State House–style event reported by The Point described Jah presenting two new Mercedes-Benz vehicles to Jammeh and explicitly framed the gesture as a birthday gift. The same report quoted officials praising Jah’s support, while Jah himself reportedly attributed his progress to presidential empowerment. That is not a neutral distance from authoritarian power; it is public reciprocity signaling. [The Point, June 2013]

To contextualize why these matters, the TRRC White Paper, Human Rights Watch reporting on the commission, and Transparency International’s corruption overview all depict the Jammeh system as authoritarian, violent, and deeply patrimonial. Those sources do not constitute a legal finding against Jah. But they establish the character of the regime within which he publicly aligned himself. So the cleanest formulation is this: there is strong evidence of Jah’s public support for an authoritarian incumbent, and weak evidence that he positioned himself with democratic resistance or an oppositional business class during that era. [TRRC White Paper/Ministry of Justice; Human Rights Watch; Transparency International]

After regime change, the pattern did not break; it reconfigured. In November 2017, Barrow inaugurated QCity and praised Jah’s investment as development-friendly. In political-economy language, that is a move from authoritarian embeddedness to democratic-era relational contracting. The mechanism changes, but the core logic remains: large domestic capital receives symbolic state endorsement and, in return, becomes legible as a partner in national development. This is how discretionary states reproduce concentrated business power across political transitions. [State House release, Nov. 30, 2017]

Case Studies in State-Business Reciprocity

The first case study is the QCell licensing story. PURA’s 2009 annual report states that QCell entered in July 2009 and received the first 3G GSM license on July 7, 2009. Later, PURA publicly endorsed 5G deployment after consultation and testing. Neither decision is inherently improper. But in a country where the World Bank has warned that regulatory independence is constrained and vulnerable to political influence, repeated frontier-positioning by the same business group deserves scrutiny. The relevant economic concern is not simply favoritism; it is dynamic foreclosure: early preferential positioning can compound into enduring advantage through brand effects, coverage externalities, and customer lock-in. [PURA Annual Report 2009; PURA 5G public notice; World Bank Digital Economy Diagnostic]

The second case study is the 2017 QCity/QTV moment. Barrow’s public inauguration of a Jah-linked project shortly after the democratic transition matters because it illustrates regime continuity in business mediation. The state can project openness while still channelling visibility and legitimacy toward already-connected actors. QTV’s existence alongside QCell also magnifies the issue. Cross-sector ownership between telecom and broadcast assets can increase bargaining power over advertising, narrative framing, and soft influence, even if no single market is monopolized. A privately owned TV station need not behave as a crude propaganda machine to matter politically; it merely needs to know where its owner’s broader portfolio benefits lie. [State House release, Nov. 30, 2017; PURA broadcasting registry]

The third case study is the 2024–2025 procurement-financing sequence. In 2024, the finance minister told the National Assembly that 89 OIC-related vehicles were purchased from Espace Motors and that the supplier effectively pre-financed the transaction because conventional financing was unavailable under the timeline. In 2025, Jah defended a KMC truck deal, explaining that the customary 20 percent advance payment requirement was waived and that financing was arranged through Musharaka structures involving Espace/Quantum Net and AGIB Bank. Economically, this is the clearest window into the mechanics of connected advantage. Supplier pre-financing and waived advances can sometimes solve genuine liquidity constraints. But they also create entry barriers: only firms with sufficient political confidence, capital depth, and banking linkages can offer the state such terms. That shifts procurement from open price competition toward relationship-based intermediation. It also raises the specter of quasi-fiscal exposure, because public sector payment risk is effectively warehoused inside politically connected private balance sheets. [The Standard, Sept. 2024; The Point, 2025]

Market Structure, Concentration, and Allocative Efficiency

The empirics do not support the easy slogan that Jah already holds a literal monopoly. Freedom House reported four mobile providers and four ISPs in 2019. PURA’s 2024 reporting put Africell at 56 percent of mobile subscribers and QCell at 25 percent, leaving 19 percent for the rest of the market. QTV is one of five television content providers listed by PURA. So, the correct diagnosis is not monopoly simpliciter. It is a concentrated cross-sector presence under weak contestability. [Freedom House 2019; PURA Annual Report 2024; PURA broadcasting registry]

Using the PURA 2024 mobile figures, a rough HHI is feasible. If the residual 19 percent is split evenly across the two remaining operators, the HHI is 56² + 25² + 9.5² + 9.5² = 3,931. If instead a single remaining rival holds the 19 percent, the HHI rises to 4,122. Either way, the market is highly concentrated by standard competition thresholds. QCell is not the dominant operator, but it is still part of a concentrated oligopoly. The deeper issue is that conglomerate diversification into media, vehicles, and banking can extend influence beyond formal telecom market share. That produces portfolio power, not just market power.

Mobile market shares from public reporting

Africell

The GAMBIA: MUHAMMED JAH: THE ECONOMIC VAMPIRE